Winning the loser's game

Re: Winning the loser's game

When asked the ideal dollar figure for assets under management in Winton’s newly launched trend-following fund, David Harding’s answer prompts a double take. “Nought would be perfect”, the firm’s founder says. He is only half joking.

After 20 years, Harding is steering the $30 billion firm he built increasingly away from trend following. Winton is cutting the weight of the strategy in its main fund – the Winton Fund – by half, from 50% to around 25%.

The new launch is for clients that want to keep a higher exposure, but frankly Winton is hoping few of them do.

“It’s a significant commercial move, a significant reorientation of Winton’s resources internally and market positioning,” says Harding. It is also a big step for one of trend-following’s pioneers. Harding is the ‘H’ in AHL, the quant firm he co-founded in the late 1980s and sold to Man Group before launching Winton in the late 1990s.

He talks about “steeling” himself before making the decision. Yet this is no dramatic rift with the past, he asserts.

Trend following might have worked “fantastically well” for more than three decades, but the wane of the strategy underscores Winton’s view that “there are no immutable laws in finance”, he says.

Speaking to Risk.net in his office at Winton’s headquarters in London, Harding damns the view rooted in the work of academics Eugene Fama and Kenneth French that markets can be seen as efficient price-discovery machines where enduring rules apply – the so-called efficient market hypothesis.

“Everything we’re doing,” he says, “is centred on the ways in which efficient market theory isn’t true”.

The last straw

Harding’s long-held beliefs on market inefficiency met a more pressing reason for a change of tack during February’s market turmoil.

February was “the straw that broke the camel’s back”, Harding says, convincing him trend following had become “further overcrowded”.

“My estimate of the level of slippage caused by trend followers’ position adjustment after February edged up. And when I say ‘edged’ I mean a 10–20% increase.”

Trend-following hedge funds typically scale positions based on volatility, leading to fears about what would happen if funds were forced to cut exposures due to a sudden increase in volatility. During the first week of February, the Vix index of implied volatility in equities spiked from around 13 to 37.

At the end of the month, the S&P 500 was down close to 4%. The Winton Fund lost 5% in February and Societe Generale’s index of trend-following hedge funds posted a 6% loss, its second worst since inception in 2000.

The episode highlighted the growing difficulty of satisfying the twin objectives typical of investors in trend-following funds, Harding says – maximising risk-adjusted returns, but also minimising the correlation of the portfolio with equity markets, to which many of these investors have high exposures.

We have become famous as a trend follower. That’s a great thing. It gives you this reputation and franchise. But it’s also a bit of a prison. It’s your enemy and your friend at the same time.

David Harding

“The tension arising as a result of trying to satisfy these two masters” had become “steadily more stretched”, Harding says. “After February we decided we had to make the distinction clearer to our clients.”

Winton will reduce the weight of trend following in the Winton Fund, a multi-strategy fund that manages more than $9 billion in assets, and in other funds managing a further $3.5 billion by “about” January next year.

The new stand-alone trend-following fund has a 1% management fee and no performance charges – Harding says the returns no longer justify hedge-fund type fees. The strategy delivered roughly a 0.5 Sharpe ratio over the past 10 years, Harding estimates, versus 0.8 for the Winton Fund overall.

“We have become famous as a trend follower. That’s a great thing. It gives you this reputation and franchise. But it’s also a bit of a prison. It’s your enemy and your friend at the same time.”

Harding says he worries that “all the clients might say: ‘Oh we’ll have the thing that’s cheaper’ ” – but so far the signs are encouraging. He thinks 5–10% of assets might have switched to the new fund by year end.

Competition

A cynical reading of this could be that Winton is responding to the commoditisation of trend following by banks and asset managers offering alternative or smart-beta products.

Broadly, these lower-cost products are based on the idea that funds that systematically tilt towards securities with price momentum can harvest a lasting premium from investors’ tendency to favour winners and shun losers.

Several of Winton’s peers have responded to the competition and to sluggish sector returns by targeting new markets or offering simpler, cheaper versions of their strategies.

Man AHL has led moves into more esoteric assets, where competition is less intense and trends are arguably stronger. Aspect Capital launched a low-cost version of its trend-following strategy in 2016.

But Harding rejects absolutely the idea Winton is being undercut or that trend following can be thought of as beta at all.

Momentum is not a fixed law of markets, he says; it was a good trade and it got crowded. “If any trade gets very crowded then it can backfire,” he says. “It’s a standard market thing. If everyone tries to do the same thing at the same time it goes wrong.”

The implications for providers now looking to feed on what hitherto was Winton’s bread and butter are evident. “I expect trend following to gradually deteriorate and I’ve been on record saying that for years,” Harding says.

Equally he rejects the suggestion that because trend-following returns have waned, the opportunity for firms like Winton has shrunk. Such thinking comes from the flawed assumption that markets fit the efficient market model, he says.

Here Harding sets out his view of market returns as “in general the product of a complex, multidimensional chaotic process” impossible to characterise by any simple mathematical model. Once he hits his stride on the topic, there is little stopping him.

“The track record of firms such as Winton and AHL over the last 30 years is a living refutation of the efficient market hypothesis put forward by Fama and French,” he says. “Seeing your hypothesis falsified and then trying to defend it by retrospectively introducing extra variables and fitting the data to them is hardly the height of good scientific practice.”

The idea of markets as efficient can be useful in the same way as Newtonian physics is useful, he says. But losing sight of the theory’s flaws risks allowing dogma to stand in the way of progress. “It’s a set of intellectual ideas that, if I were being really critical, I’d say forestalls all thought.

“There are no laws of finance. Many people in finance seem to be trying to treat it as a physical science. This is a mistaken approach. Their philosophy is wrong.”

The Winton way

These views inform Winton’s investment approach in some intriguing ways.

For one, it means championing the value of wisdom in investing. Harding references Warren Buffett several times as an example of someone with an admirably broad base of knowledge. Charlie Munger’s book On Success shows he is “incredibly widely read”, Harding says.

The quant culture in finance, conversely, he sees as often dogmatic. “Many mathematicians and programmers don’t read a lot of history, philosophy, religion,” Harding says. “That’s what you need to be a successful investor. You need to have an eclectic outlook on the world.”

Secondly, Harding is not hung up on the interpretability of signals.

“If I could find strong evidence in some data that there was a phenomenon we could make money from, I wouldn’t care whether I understood it or not.”

People always say to me: ‘This is what works.’ I say: ‘Worked’

David Harding

As a hypothetical example he suggests the Bank of Japan might rebalance its foreign currency reserves at the same time each week. “You might find that anomaly, find that it is as strong as hell,” Harding says. “You don’t know why it works. But you can make money out of it.”

A third point of influence is Winton’s insistence on the stringent testing of ideas.

Strong evidence of a tradeable signal requires more than “running a five dimensional optimisation back over the data” and getting a strong result, Harding says.

“People always say to me: ‘This is what works.’ I say: ‘Worked’.

“‘Works’ implies a property of a population. ‘Worked’ implies it is the property of a sample. ‘Works’ implies this is a fundamental underlying property of nature. ‘Worked’ implies it might have been significant or might simply have been a random feature of the data.”

As for the future, Harding sees no comparative advantage in seeking out strong signals which mostly will be quickly identified and traded on by others. Instead, Winton’s focus is on continuing to seek out weak signals but more of them.

“For weak signals there’s relatively little time and effort devoted to looking for them by others,” Harding says. The approach, which leads Winton to draw its researchers often from academic disciplines where the problems of using data with low signal-to-noise ratios are well understood, has served the firm well.

Winton’s full-year return for 2017 was 7.9%, compared with less than 2.5% for SocGen’s index that tracks funds with a purer focus on trend following. The Winton Fund is up 2.5% net year-to-date, whereas the SocGen index has lost more than 4%.

In other commercial moves, Winton has successfully registered with the Asset Management Association of China as a private securities investment fund manager, enabling the firm to develop onshore investment products for qualified investors in China.

The firm also recently span off its Hivemind data science unit to run as a stand-alone business. Harding describes Winton’s core skill as “using powerful computers to look for empirical patterns and relationships in data” and the company describes itself as an investment management and data science company, possibly pointing to more ventures in areas beyond finance.

Winton already invests in businesses in fields such as cybersecurity and healthcare where data science is set to play a pivotal role in future.

As for Winton’s core business, though, the impression Harding leaves is clear: he is not regretful about decoupling from the strategy that made his reputation.

“When Mick Jagger gets up on stage he’s always got to play Paint it Black and Brown Sugar,” he jokes. “We’ve had to play Paint it Black and Brown Sugar over and over again.”

https://www.winton.com/news/2018/risk-n ... -following

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

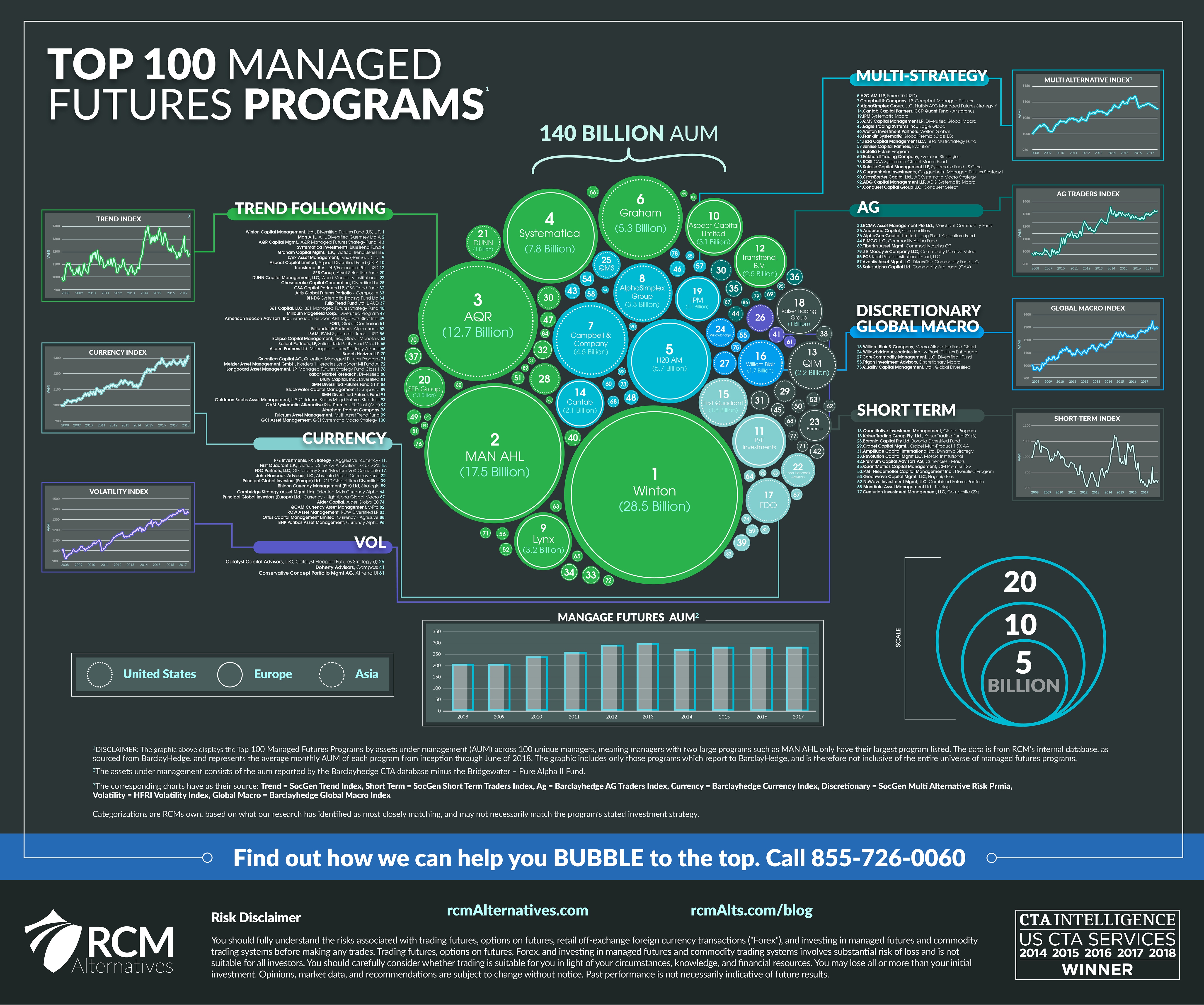

We show the top 100 unique Managed Futures programs by their average monthly assets under management from inception through the end of last year. The programs part means you won’t see AQR with 20+ billion, as we’re only considering their managed futures program, not the firm overall. Likewise, the unique part means you won’t see Man AHL’s flagship program and their newer Evolution program – which are both within the top 20. We further grouped this list by strategy type, and again by geographic location to get an idea of what the breakdown of assets looks like among these titans.

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Jonhy_Rico Escreveu:Ações

Vanguard Total World Stock Index Fund ETF Shares VT

iShares Core MSCI World UCITS ETF SWDA

O primeiro é americano e distribui dividendos. Logo, o 2.º, é muito melhor para um investidor europeu, mau grado o fee de gestão ser ligeiramente superior.

Jonhy_Rico Escreveu:Obrigações

iShares Core € Govt Bond UCITS ETF IEGA

iShares Core € Corp Bond UCITS ETF IEAC

Ambos os ETFs distribuem dividendos. De um ponto de vista fiscal, são ineficientes.

Se queres um razoável (não existem bons!) ETF de obrigações soberanas europeias, com uma maturidade média de 5 a 7 anos, sugiro o seguinte: LU1287023003

Pessoalmente não invisto em obrigações corporativas, nem invisto em obrigações mundiais sem ter cobertura cambial.

Jonhy_Rico Escreveu:Tenho de me preocupar com cobertura cambial?

Não, se investires no iShares Core MSCI World e no Lyxor EuroMTS 5-7Y Investment Grade (DR) UCITS ETF C-EUR.

Nota, se estás mesmo interessado em ter cobertura cambial para as acções mundiais, compara esse ETF com a sua versão com hedge cambial: IE00B441G979

Jonhy_Rico Escreveu:Posso comprar isto pelo Banco Best ou recomendam considerar outra corretora?

No Best, apenas tens acesso ao iShares Core MSCI World. Mas na degiro suponho que encontres os outros ETFs acima.

Jonhy_Rico Escreveu:Nas ações escolheria apenas um daqueles fundos. Dado que o primeiro é mais barato e já inclui small caps suponho que seja uma melhor opção, correto?

Ver acima.

- Mensagens: 379

- Registado: 13/9/2013 0:16

Re: Winning the loser's game

Olá pessoal.

Desta vez estou a procura de ajuda para preparar uma carteira de investimento em Portugal.

A ideia é construir uma carteira super simples de 2 a 4 ETFs para investir a 7-10 anos com reforços anuais e com um foco em gestão passiva e baixos custos. Possivelmente será metade ações e metade obrigações, mas ainda estamos a ponderar ser 70/30.

Algumas das opções que encontrei:

Ações

Vanguard Total World Stock Index Fund ETF Shares VT

iShares Core MSCI World UCITS ETF SWDA

Obrigações

iShares Core € Govt Bond UCITS ETF IEGA

iShares Core € Corp Bond UCITS ETF IEAC

Questões:

Existem ETFs mais indicados que estes?

Tenho de me preocupar com cobertura cambial?

Posso comprar isto pelo Banco Best ou recomendam considerar outra corretora?

Nas ações escolheria apenas um daqueles fundos. Dado que o primeiro é mais barato e já inclui small caps suponho que seja uma melhor opção, correto?

Desta vez estou a procura de ajuda para preparar uma carteira de investimento em Portugal.

A ideia é construir uma carteira super simples de 2 a 4 ETFs para investir a 7-10 anos com reforços anuais e com um foco em gestão passiva e baixos custos. Possivelmente será metade ações e metade obrigações, mas ainda estamos a ponderar ser 70/30.

Algumas das opções que encontrei:

Ações

Vanguard Total World Stock Index Fund ETF Shares VT

iShares Core MSCI World UCITS ETF SWDA

Obrigações

iShares Core € Govt Bond UCITS ETF IEGA

iShares Core € Corp Bond UCITS ETF IEAC

Questões:

Existem ETFs mais indicados que estes?

Tenho de me preocupar com cobertura cambial?

Posso comprar isto pelo Banco Best ou recomendam considerar outra corretora?

Nas ações escolheria apenas um daqueles fundos. Dado que o primeiro é mais barato e já inclui small caps suponho que seja uma melhor opção, correto?

-

- Mensagens: 96

- Registado: 18/7/2014 8:38

Re: Winning the loser's game

Jonhy_Rico Escreveu:Boas,

Tenho uma carteira de ETFs na Austrália (onde sou Residente Permanente) muito simples constituida da seguinte forma:

35% VAS (100% ações Australianas). Comissão de gestão 0.14%

35% VGS (100% ações de todo mundo, exceto Australia; maior peso nos EUA). Comissão de gestão 0.18%

30% VAF (100% fixed income Australia). Comissão de gestão 0.20%

Todos eles são transacionados no ASX e uma vez por ano compro os 3 para adicionar a minha carteira de longo prazo, mantendo essas percentagens. Essa operação custa-me 11$ por trade (33$ no total por ano).

A Vanguard Australia agora lançou um ETF novo que basicamente faz o que esses 3 fazem e mais, e com mais diversificação e alguma cobertura cambial.

VDGR (70% ações, 30% Fixed Income). Comissão de gestão 0.27%

Growth assets

Vanguard Australian Shares Index Fund (Wholesale) 28%

Vanguard International Shares Index Fund (Wholesale) 18.5%

Vanguard International Shares Index Fund (Hedged) - AUD Class (Wholesale) 12.5%

Vanguard International Small Companies Index Fund (Wholesale) 5%

Vanguard Emerging Markets Shares Index Fund (Wholesale) 4%

Income assets

Vanguard Global Aggregate Bond Index Fund (Hedged) 21%

Vanguard Australian Fixed Interest Index Fund (Wholesale) 9%

Se eu optar por alterar para esta opção alternativa tenho uma comissão de gestão mais alta, mas com apenas uma transação anual de 11$.

Também fico com a carteira mais diversificada e com mais cobertura cambial, mas teria de executar mais valias na minha carteira atual e ser taxados nessas mais valias, o que me parece uma desvantagem.

Se fossem vocês, o que fariam?

Mantinha a que já tinha e iniciava uma nova com o tal ETF.

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Boas,

Tenho uma carteira de ETFs na Austrália (onde sou Residente Permanente) muito simples constituida da seguinte forma:

35% VAS (100% ações Australianas). Comissão de gestão 0.14%

35% VGS (100% ações de todo mundo, exceto Australia; maior peso nos EUA). Comissão de gestão 0.18%

30% VAF (100% fixed income Australia). Comissão de gestão 0.20%

Todos eles são transacionados no ASX e uma vez por ano compro os 3 para adicionar a minha carteira de longo prazo, mantendo essas percentagens. Essa operação custa-me 11$ por trade (33$ no total por ano).

A Vanguard Australia agora lançou um ETF novo que basicamente faz o que esses 3 fazem e mais, e com mais diversificação e alguma cobertura cambial.

VDGR (70% ações, 30% Fixed Income). Comissão de gestão 0.27%

Growth assets

Vanguard Australian Shares Index Fund (Wholesale) 28%

Vanguard International Shares Index Fund (Wholesale) 18.5%

Vanguard International Shares Index Fund (Hedged) - AUD Class (Wholesale) 12.5%

Vanguard International Small Companies Index Fund (Wholesale) 5%

Vanguard Emerging Markets Shares Index Fund (Wholesale) 4%

Income assets

Vanguard Global Aggregate Bond Index Fund (Hedged) 21%

Vanguard Australian Fixed Interest Index Fund (Wholesale) 9%

Se eu optar por alterar para esta opção alternativa tenho uma comissão de gestão mais alta, mas com apenas uma transação anual de 11$.

Também fico com a carteira mais diversificada e com mais cobertura cambial, mas teria de executar mais valias na minha carteira atual e ser taxados nessas mais valias, o que me parece uma desvantagem.

Se fossem vocês, o que fariam?

Tenho uma carteira de ETFs na Austrália (onde sou Residente Permanente) muito simples constituida da seguinte forma:

35% VAS (100% ações Australianas). Comissão de gestão 0.14%

35% VGS (100% ações de todo mundo, exceto Australia; maior peso nos EUA). Comissão de gestão 0.18%

30% VAF (100% fixed income Australia). Comissão de gestão 0.20%

Todos eles são transacionados no ASX e uma vez por ano compro os 3 para adicionar a minha carteira de longo prazo, mantendo essas percentagens. Essa operação custa-me 11$ por trade (33$ no total por ano).

A Vanguard Australia agora lançou um ETF novo que basicamente faz o que esses 3 fazem e mais, e com mais diversificação e alguma cobertura cambial.

VDGR (70% ações, 30% Fixed Income). Comissão de gestão 0.27%

Growth assets

Vanguard Australian Shares Index Fund (Wholesale) 28%

Vanguard International Shares Index Fund (Wholesale) 18.5%

Vanguard International Shares Index Fund (Hedged) - AUD Class (Wholesale) 12.5%

Vanguard International Small Companies Index Fund (Wholesale) 5%

Vanguard Emerging Markets Shares Index Fund (Wholesale) 4%

Income assets

Vanguard Global Aggregate Bond Index Fund (Hedged) 21%

Vanguard Australian Fixed Interest Index Fund (Wholesale) 9%

Se eu optar por alterar para esta opção alternativa tenho uma comissão de gestão mais alta, mas com apenas uma transação anual de 11$.

Também fico com a carteira mais diversificada e com mais cobertura cambial, mas teria de executar mais valias na minha carteira atual e ser taxados nessas mais valias, o que me parece uma desvantagem.

Se fossem vocês, o que fariam?

-

- Mensagens: 96

- Registado: 18/7/2014 8:38

Re: Winning the loser's game

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

The S&P 500 Index has recorded more than 150 new all-time highs since eclipsing its previous peak in late March of 2013. In 2017 alone, there have been 30 new record highs through the end of last week. To put this into perspective, there were only 13 new highs for the entire decade of the 2000s.

When you combine a stock market that continues to see so many new highs with above-average valuations, investors get worried. One of these peaks will be the peak, but predicting that ahead of time is not easy. Life would be much easier if there were more bargains available and higher interest rates, but we have to invest in the markets as they are, not as we wish they could be.

Here are some options:

Rebalance. A simple portfolio that started out 2009 with 60 percent in U.S. stocks and 40 percent in U.S. bonds would now have close to 80 percent in stocks and 20 percent in bonds. Going from a 60/40 portfolio to an 80/20 portfolio is a huge change in risk profile and loss potential. There’s no reason to set target asset allocation weights if you’re not going to periodically rebalance back to your preset amounts on occasion.

Over-rebalance. If you’re nervous about stocks, you could put more money in underperforming assets. Value stocks have underperformed growth stocks by more than 3 percentage points annually over the past 10 years. The relative performance is even worse overseas. U.S. stocks have outperformed European stocks by 29 percent, 44 percent and 100 percent over the past three-, five- and 10 year periods. U.S. stocks have outperformed emerging markets by 28 percent, 73 percent and 91 percent over those same intervals. Investors looking to take advantage of mean reversion could allocate more of their portfolios to value and international stocks.

Avoid complexity. Someone is going to be a hero coming out of the next market downturn, but figuring out who that will be is like playing the lottery. There are plenty of complex hedging techniques, bear market funds, leveraged ETFs and VIX products you can invest in, but most require incredible foresight to work. You can be “right” in the markets and still not make any money, as mistimed trades, volatility and costs can often eat up good investment ideas. The easiest way to hedge risk in the markets is to simply take less risk by raising more cash or investing in more high-quality bonds and fewer equities.

Have enough cash to make it through a rainy year or three. One of the worst positions to be in as an investor is being a forced seller of your shares at an inopportune time. You give yourself a margin of safety by having enough cash on hand in safe holdings to see you through a disruption in the markets or economy. Low interest rates mean you won’t earn much on your cash holdings, but the peace of mind in knowing you can meet your expenses in a downturn is worth more than a few percentage points in returns. This money can also be used as dry powder when the next downturn comes around.

DCA and diversify. From a psychological standpoint, there are few strategies that work better than dollar cost averaging into a diversified portfolio of assets. This isn’t a strategy you can brag about to your friends, but making investment contributions at periodic intervals regardless of price is one of the simplest ways to avoid making mistakes or over-thinking investment decisions.

Buy and hold. To paraphrase Winston Churchill, buy and hold is the worst investment strategy, except for all the others. Being a long-term investor is easy when things are going up. But to be a true buy-and-hold devotee, you have to both buy and hold when things are going down, as well. This is not for everyone because it’s emotionally challenging, but it is a great way to decrease transaction costs, taxes and market timing errors.

Embrace the momentum. One of the hardest things to wrap your head around as an investor is that all-time highs in stocks are typically followed by more all-time highs. One way to take advantage of this is by investing in momentum or trend-following strategies. Momentum is based on the idea that assets that have performed relatively well (or poorly) recently will continue to perform well (or poorly) going forward, at least for a short period of time, because markets can be irrational in the short run. These strategies have been proven to work but typically require a rules-based framework to keep the emotions out of the equation.

Each of these approaches has its drawbacks, but there are no perfect investment strategies. The best thing you can do as an investor is to pick the one that works for you from a psychological standpoint. Even the greatest investment strategy in the world is pointless if you can’t stick with it.

https://www.bloomberg.com/view/articles ... rket-peaks

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Black Monday: Simulation of a Trend-Following System

https://www.youtube.com/watch?time_cont ... iLb1a_G5LY

by David Harding

https://www.youtube.com/watch?time_cont ... iLb1a_G5LY

by David Harding

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Foi só uma dúvida que me surgiu. Daquelas que ao longo do tempo vai-nos surgindo e que pensamos ser importante

De facto não vou inventar nada e se os USA valem X% é isso que deveremos manter obviamente independentemente de pensar isto ou aquilo.

Obrigado pelas respostas mouro e já agora ficamos todos a aguardar o teu feedback sobre os resultados da tua carteira ficticia

De facto não vou inventar nada e se os USA valem X% é isso que deveremos manter obviamente independentemente de pensar isto ou aquilo.

Obrigado pelas respostas mouro e já agora ficamos todos a aguardar o teu feedback sobre os resultados da tua carteira ficticia

- Mensagens: 289

- Registado: 8/3/2014 19:34

Re: Winning the loser's game

ZeNovato Escreveu:http://thereformedbroker.com/2017/05/24/what-were-telling-clients-about-european-stocks/

Eu li este site que foi deixado noutro fórum e fiquei a pensar o seguinte.....

Ora se a nível mundial os USA tem 60% do mercado mas têm o mesmo retorno que a europa no longo prazo, do meu ponto de vista estamos a introduzir um maior risco ao aceitarmos os 60%, certo (mesmo a nível cambial)?

Se dizemos que a logo prazo, os USA e europa têm retornos de cerca de 9% então a diferença entre ter 60%/40% entre USA/EUR ou deter 50%/50% USA/EUR em termos de retornos a longo prazo iria dar ao mesmo não?

Bem sei que é filme da minha parte e não sou eu quem vai inventar seja o que for mas pronto.....

Acho que estás a complicar.

Se os 60% dos EUA e os 20% da UEE terão o mesmo retorno esperado a longo prazo (it's an estimate!), se te desviares dessas percentagens, apenas estarás a aumentar o risco do retorno no final ser enviesado (tanto para cima, como para baixo). Nota, ninguém sabe o futuro.

Volto a dizer, uma gestão passiva de longo-prazo buy&hold não se deveria preocupar muito com isso, nem perder demasiado tempo a estudar isso.

Mais vale perder tempo a estudar a sério (sim, qualificações para aumentar o salário!). Mais vale ter um salário de 2.000 Euros que renda 2% ao ano, do que ter um salário de 1.000 Euros que renda 6% ao ano,

- Mensagens: 379

- Registado: 13/9/2013 0:16

Re: Winning the loser's game

http://thereformedbroker.com/2017/05/24 ... an-stocks/

Eu li este site que foi deixado noutro fórum e fiquei a pensar o seguinte.....

Ora se a nível mundial os USA tem 60% do mercado mas têm o mesmo retorno que a europa no longo prazo, do meu ponto de vista estamos a introduzir um maior risco ao aceitarmos os 60%, certo (mesmo a nível cambial)?

Se dizemos que a logo prazo, os USA e europa têm retornos de cerca de 9% então a diferença entre ter 60%/40% entre USA/EUR ou deter 50%/50% USA/EUR em termos de retornos a longo prazo iria dar ao mesmo não?

Bem sei que é filme da minha parte e não sou eu quem vai inventar seja o que for mas pronto.....

Eu li este site que foi deixado noutro fórum e fiquei a pensar o seguinte.....

Ora se a nível mundial os USA tem 60% do mercado mas têm o mesmo retorno que a europa no longo prazo, do meu ponto de vista estamos a introduzir um maior risco ao aceitarmos os 60%, certo (mesmo a nível cambial)?

Se dizemos que a logo prazo, os USA e europa têm retornos de cerca de 9% então a diferença entre ter 60%/40% entre USA/EUR ou deter 50%/50% USA/EUR em termos de retornos a longo prazo iria dar ao mesmo não?

Bem sei que é filme da minha parte e não sou eu quem vai inventar seja o que for mas pronto.....

- Mensagens: 289

- Registado: 8/3/2014 19:34

Re: Winning the loser's game

ZeNovato Escreveu:Será que alguém me poderia esclarecer uma dúvida que surgiu.

Vou pegar por exemplo no etf IWDA que sendo ações globais tem a sua distribuição pela importância dos mercados (dai estar com 60% em USA).

A minha dúvida é a seguinte:

Será que diminuíamos o risco se usássemos uma distribuição igual em percentagem pelas zonas geográficas mundiais onde teríamos os 100% da componente ações distribuída em 25% por USA; EUR; Asia; Emerg.

Ainda mais se, não fazendo hedge das ações, será que havia uma distribuição mais igualitária no que respeita às moedas?

O mercado acionista por zona geográfica deverá ter mais ou menos a mesma performance no longo prazo.

Historicamente, os melhores trackers são os trackers "market-cap". Se a capitalização bolsista é de 60% nos EUA, ao alocares apenas 25% à tua carteira, estás-te a desviar (bastante) do mercado.

Quer isso dizer que achas que sabes mais do que o mercado, uma vez que o mesmo é (tendencialmente) eficiente.

Não quer dizer que não possam existir índices equal-weight ou country-weight que, nos últimos tempos, tenham tido um melhor desempenho do que os índices "market-cap". Mas mais uma vez, acertar no euromilhões à 4ª Feira é muito fácil.

No que respeita ao hedge cambial, mais uma vez, tendencialmente no longo-prazo as moedas tendem para um equilíbrio. Nota, parte dos lucros mundiais da Coca-Cola são numa moeda que não o USD. Naturalmente, a sua cotação em USD leva isso em consideração.

Por outras palavras, o hedge cambial só faria sentido se as empresas fossem exclusivamente regionais: Coca-Cola apenas venderia nos EUA, a VW na Europa, a BP no Reino Unido, a Toyota no Japão, etc.

- Mensagens: 379

- Registado: 13/9/2013 0:16

Re: Winning the loser's game

Será que alguém me poderia esclarecer uma dúvida que surgiu.

Vou pegar por exemplo no etf IWDA que sendo ações globais tem a sua distribuição pela importância dos mercados (dai estar com 60% em USA).

A minha dúvida é a seguinte:

Será que diminuíamos o risco se usássemos uma distribuição igual em percentagem pelas zonas geográficas mundiais onde teríamos os 100% da componente ações distribuída em 25% por USA; EUR; Asia; Emerg.

Ainda mais se, não fazendo hedge das ações, será que havia uma distribuição mais igualitária no que respeita às moedas?

O mercado acionista por zona geográfica deverá ter mais ou menos a mesma performance no longo prazo.

Vou pegar por exemplo no etf IWDA que sendo ações globais tem a sua distribuição pela importância dos mercados (dai estar com 60% em USA).

A minha dúvida é a seguinte:

Será que diminuíamos o risco se usássemos uma distribuição igual em percentagem pelas zonas geográficas mundiais onde teríamos os 100% da componente ações distribuída em 25% por USA; EUR; Asia; Emerg.

Ainda mais se, não fazendo hedge das ações, será que havia uma distribuição mais igualitária no que respeita às moedas?

O mercado acionista por zona geográfica deverá ter mais ou menos a mesma performance no longo prazo.

- Mensagens: 289

- Registado: 8/3/2014 19:34

Re: Winning the loser's game

Finding the Active in Low-Cost Passive Investing

https://www.bloomberg.com/view/articles ... -investing

Hence, passive does reflect a number of choices, made over time. This is why some of the pioneers of indexing -- Charlie Ellis, former chairman of the Yale University endowment, comes to mind -- prefer the phrase "low-cost indexing” rather than passive investing. You should, too.

https://www.bloomberg.com/view/articles ... -investing

- Mensagens: 379

- Registado: 13/9/2013 0:16

Re: Winning the loser's game

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

It’s far from clear risk-parity and CTA funds react to the same set of inputs. While both invest in multiple asset classes and employ leverage, risk parity tends to be a slower and more passive strategy, aiming to engineer a smoother ride by giving smaller weightings to higher-volatility assets. CTAs, a type of managed futures strategy, follows short-term trends and tends to be more volatile and less correlated to the market.

Risk parity would only unload positions quickly if managers kicked in some type of stop loss, which only a few do, according to Croce.

That may be true for the biggest players, but doesn’t account for the actions of a less illustrious category of risk parity funds, many of which have started to unwind, according Brean Capital LLC’s Peter Tchir.

“I don’t think this move has caused much of an unwind from true risk parity funds, but much more from the homebrew or risk parity lite crowd -- making the real fun just beginning,” Tchir wrote in a note Thursday. “Risk parity selling should kick in when expected volatility of the strategy exceeds target volatility of the strategy.”

As employed like Bridgewater Associates LP’s All Weather Fund, risk parity holds consistent levels of exposures. When it rebalances, the fund buys assets that have fallen and sells ones which have gained -- hardly a recipe for disaster. AQR Capital Management LLC does use a risk management strategy to gradually reduce exposure when returns are very poor, but that hasn’t kicked in all year, according John Huss, a portfolio manager on the risk parity team.

“We’re not trying to chase one day or one week moves,” Huss said. “When there are larger shifts in exposure, like the way we were positioned in 2008 versus 2012 with really noticeable changes in size, they tend to happen more slowly over time.”

CTAs may be a bigger threat. They’re large -- Barclays PLC estimates them to be about 7 percent of hedge fund industry assets -- and react quickly. Take $1.4 billion Quest Partners LLC, which runs mostly managed futures funds. Before last week the firm was mostly long Treasuries, and has already flipped to a short position, according to Nigol Koulajian, co-founder and chief investment officer.

Last week’s pain wasn’t as clear cut as a selloff in fixed income for some trend-followers. The managed futures fund at Salient, for example, suffered from a short position in agricultural commodities after wheat futures rallied to four-year highs.

“Momentum trading can create systemic risks. CTAs are a good example, they’ll ride the trend up and ride the trend down,” said Maneesh Shanbhag, who co-founded $500 million Greenline Partners LLC after five years at Bridgewater. “Connecting that to risk parity, the more basic idea will not cause instability in markets. But a levered risk parity strategy is at risk of all asset classes falling.”

On the surface, it’s strange that both strategies suffered over the past week since they’re supposed to behave differently. A classic risk parity strategy is always long fixed income, equities and inflation risk assets. But as momentum threw its weight behind stocks and bonds, many CTAs took a similar long position.

It gets worse zeroing in on CTAs: about half of the assets are controlled by 10 managers, who are about 98 percent correlated, meaning same-way bets will indeed affect the market, according to Quest’s Koulajian.

“CTAs who have adapted to this market environment are trading more and more long-term, and their position sizing has grown,” Koulajian said. “Many people are using exactly the same strategy, and as there’s a reversal in trends, they’re impacting the market significantly.”

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Viva,

Por acaso alguém recomenda algum ETF semelhante ao BND, mas que seja de acumulação de dividendos ?

Obrigado

Bons Negocios

Por acaso alguém recomenda algum ETF semelhante ao BND, mas que seja de acumulação de dividendos ?

Obrigado

Bons Negocios

- Mensagens: 203

- Registado: 11/5/2007 22:56

- Localização: Quarteira

Re: Winning the loser's game

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18

Re: Winning the loser's game

De facto estou curioso para ver o comportamento da carteira do LTCM se o € arrancar.

Não terá qualquer impacto nas rentabilidades que viste. A carteira é feita em USD com activos em USD.

Com o avançar dos anos, o que ontem parecia muito bom, hoje pode não o ser. A evolução dos ETF's foi grandita (para não dizer enooorme). Leio por aqui e por ali que pessoas que inicialmente tinham a carteira parecida com a sugerida neste tópico avançaram para uma mais simples onde incluem p.ex o IWDA em vez de dividir por 4 ETF's.

Como tu uma vez disseste no teu tópico (acho que na pg 102) a carteira apresentada pelo LTCM é uma evolução muito grande, mas os tempos são outros.

Estou certo que disse que a realidade é outra, mas não em relação às carteiras/lazy Portfolios mas sim devido a serem carteiras em USD para americanos. A nossa realidade é outra porque faço compras em euros não em USD e não pretendo ter os meus investimentos todos em USD.

De resto concordo a 100% com o LTCM, até porque 4 ou 5 anos nada mudam em carteiras testadas ou com décadas de existência. 4.5% está mais ou menos em linha com o Permanent Portfolio, que é uma carteira com uma teoria bastante boa por detrás e com milhões de pessoas que a usam, para além de ter mais de 4 décadas. A perspectiva de ETFs e lazy portfolio é mesmo a estratégias não perderem valor com o tempo. A estratégia que uma pessoa com as mesmas características (idade, condição económica, nível de apetite de risco etc etc) deve ser a mesma em 2000 ou em 2030.

Acredita que o LTCM não nos deixou de presentear com o seu conhecimento. De vez em quando deixa aí boa pérolas, mesmo que sejam "escritos" por outras pessoas

Artigos e estudos: Página repositório dos meus estudos e análises que vou fazendo. Regularmente actualizada. É costume pelo menos mais um estudo por semana. Inclui a análise e acompanhamento das carteiras 4 e 8Fundos.

Portfolio Analyser: Ferramenta para backtests de Fundos e ETFs Europeus

"We don’t need a crystal ball to be successful investors. However, investing as if you have one is almost guaranteed to lead to sub-par results." The Irrelevant Investor

Portfolio Analyser: Ferramenta para backtests de Fundos e ETFs Europeus

"We don’t need a crystal ball to be successful investors. However, investing as if you have one is almost guaranteed to lead to sub-par results." The Irrelevant Investor

-

- Mensagens: 5707

- Registado: 20/11/2002 21:56

- Localização: Porto

-

- Mensagens: 90

- Registado: 24/2/2017 13:53

Re: Winning the loser's game

Rick Lusitano (New) Escreveu:Adivinhem quem é o único não profissional financeiro no top dos melhores consultores financeiros em 32 países, que aparece em publicações internacionais sobre fundos e gestão de activos:

O artigo em Português, na Funds People Portugal:

http://pt.fundspeople.com/news/nomes-dos-selecionadores-e-consultores-financeiros-cujos-conselhos-sobre-fundos-importa-ter-em-conta

PS: Por favor, não entrar em discussões sobre gestão activa vs. passiva, só porque estes gestores batem os ETFs passivos que servem de referência.

Remember the Golden Rule: Those who have the gold make the rules.

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

***

"A soberania e o respeito de Portugal impõem que neste lugar se erga um Forte, e isso é obra e serviço dos homens de El-Rei nosso senhor e, como tal, por mais duro, por mais difícil e por mais trabalhoso que isso dê, (...) é serviço de Portugal. E tem que se cumprir."

-

- Mensagens: 3030

- Registado: 28/2/2007 14:18